Sun

Residential Investment as a Share of GDP

The hottest dinner table conversation in Canada these days is, of course, real estate. Bubble or no bubble? Most economists keep reassuring nervous households that this time things are different and the fundamentals of the housing market are much healthier than they were 1 5 years ago. That might be true, but what is lost in this discussion is the fact that even a soft landing in the housing market will not be gentle on the economy.

Never before have we seen the housing market contributing so much to overall economic growth. Consider the following facts: Direct investment in real estate as a share of GDP is approaching the 1 989 level; Refinancing activity is at a record-high with 60% of all Canadian mortgages negotiated over the past two years—saving households roughly 10% of the annual carrying cost of a home; Borrowing against home equity rose by a record-high of 25% last year, adding close to $30 billion in cash to consumer wallets; The housing wealth effect has led to $10 billion in extra spending

last year and $25 billion over the past three years; Each home purchased last year generated almost $25,000 in extra spending (that is beyond the actual cost of the house); Construction spending is now at a record-high of $30 billion with 50% of homeowners taking on home renovations in the past two years; Employment in the construction sector rose by 4.7% since the beginning of the year—six times the rate seen in the economy as a whole.

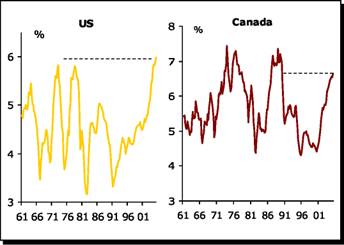

We estimate that these indirect spin-off benefits from the booming housing market have added well over half a percentage point to overall GDP growth in the past 12 months. The problem is that a leveling off in the housing market means that these benefits will not be available in 2006. That the housing market operates at a record-level makes nice newspaper headlines, but it has little economic significance. In economics almost everything is determined at the margin. What counts is the change in activity, not the level. And here there are many reasons to believe that the housing market is in the early stages of leveling off. Residential real estate investment is very close to its “resistance” level of just over 7% of GDP (Chart), housing starts are now falling, MLS resale activity during the first half of the year rose by only 1 .4% vs. the same period in 2004.

While this does not mean that the housing market is “correcting”, it means that the widely expected soft landing in real estate activity will eliminate a significant chunk of economic growth. All of the sudden the economy will not be operating so close to capacity, as feared by the Bank of Canada.

Benjamin Tal, Senior Economist