Letting go of those hard-earned property investments must be accomplished, financial advisers say

Michael Kane

Sun

CREDIT: Glenn Baglo, Vancouver Sun Chartered accountant Melanie Frers (left) gives the good news to Debbie and Dennis Nisbet: They will be financially comfortable in retirement.

Dennis and Debbie Nisbet are the classic millionaires next door. They’ve made a pile of money by investing in real estate while living modestly and making sacrifices. Now they find it hard to start spending.

The two realtors sought a free Vancouver Sun money makeover, courtesy of the Chartered Accountants of B.C., to get a handle on their retirement options.

With a $1.4-million waterfront home in Port Moody and eight rental properties, it is no surprise that Debbie, 48, and Dennis, 49, can afford to retire when they are 55.

Their big challenge is letting go of one or two of the golden hens that have built their fortune.

“I am passionate about investing in real estate to build wealth,” said Dennis. “I look at the income it could create and wonder why not just keep the properties? It is hard to transition from ‘don’t sell’ to ‘sell.’ “

However, chartered accountant Melanie Frers tells the pair they must make that transition because most of their wealth comes from the growth in the value of their real estate, rather than the rental income, which is primarily used to fund about $1.3 million in mortgages.

“You don’t want to be 90 years old and living in a basement suite with no heat and have all this property,” Frers said. “The properties are supposed to work for you. This is your retirement money.”

Although they also have about $150,000 in registered retirement savings plans and $60,000 in non-registered investments, the Nisbets have no pensions other than Canada Pension Plan.

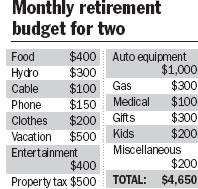

They estimate their personal retirement expenses will total $4,650 monthly ($55,800 per year), but their net rental income before tax in 2010 is estimated at $22,316, a shortfall of $33,484 plus tax.

Frers started the makeover by projecting the value of their real estate portfolio, which consists of mostly single-family homes in the Tri-Cities area and Maple Ridge.

Using a growth estimate of 7.4 per cent a year on average — based on the Nisbets’ example of a house going from $100,000 in 1980 to $600,000 in 2005 — they would net $4.45 million after tax if they sold everything, including their personal home, in 2010.

If they could invest that money at five per cent, they would earn $222,505 before tax without touching the principal. “But they would sell the home with a view which they love,” said Frers, of Port Coquitlam‘s Meyer Frers Chartered Accountants.

The real estate forecast could be derailed by a major correction in the market, and Dennis acknowledges that a 50-per-cent price appreciation is typically followed by a 25-per-cent decline. “The market tends to go two steps forward, then one step back,” he said.

If their assumptions pan out, Frers said they will need to sell one property in the year after they finish working, subject to the state of the market.

If the market is flat or down, they can use their RRSPs to fill the income gap until it bounces back, although Frers notes that their financial assets give them a more balanced investment portfolio if property values decline. As well, the tax on RRSP withdrawals will likely be higher than the tax on capital gains from real estate.

She suggests they sell their recreational property in Birch Bay, since it is the only one that does not provide any income. The property was originally acquired for $19,000 in the 1980s because it was cheaper than paying for moorage for their boat in the Lower Mainland. They now have a floating dock off their home in Port Moody.

The Birch Bay sale could be expected to generate about $200,000 in cash, which Frers suggests they invest very conservatively — earning only two per cent interest — while they draw it down to supplement their rental income.

By 2013, they will need to sell a second property, and Frers picked one expected to net $515,103 after tax and paying out the mortgage. Again, they would invest the money very conservatively and use it to supplement their rental income.

When they are 60, they can apply for reduced Canada Pension Plan, which will boost their income by an estimated $10,560 per year, and by age 67, one of their mortgages will be paid off, adding another $12,264 to their annual cash flow.

By the time they are 75, Frers anticipates that all of their mortgages will be gone and they will be more than meeting their budget without selling any more homes. They will still have seven of their nine properties and will be able to leave a large inheritance for their four adult children from previous marriages.

Frers assumes the couple will work for the next five years, and suggests they resist the temptation to purchase another rental property. They don’t need to boost their RRSPs, but if they choose to save more, she suggests they contribute to a spousal RRSP for Debbie, giving Dennis the up-front tax break while equalizing their retirement nest eggs to minimize taxes when the money is withdrawn as income.

Both Nisbets describe themselves as frugal, although they have built an enviable lifestyle based on previous sacrifices and what Dennis describes as a “nose-down, tail-up” approach whenever the real estate market turned against them.

In addition to “an older” eight-metre boat, Dennis owns a ’92 Harley motorcycle, a pre-owned car, and has built his own kit car for road racing. He raced for three years with the Honda Michelin professional series, and would love to race again when he is 60, although he says it costs a fortune.

Debbie, meanwhile, wants to do some renovations on their home, and Frers suggests she begin, using their non-registered savings to pay the bills.

Frers’ concluding advice to both of them: “Relax and enjoy your retirement.”

IN NEED OF A MAKEOVER?

You don’t need lots of money to qualify for a free Vancouver Sun Money Makeover, courtesy of the Chartered Accountants of British Columbia. We welcome candidates from all walks of life who are prepared to share their story in Smart Money and be pictured with the chartered accountant who provides their makeover. For an application form, please send your name, address and telephone number to Michael Kane at [email protected]; or fax 604-605-2320; or c/o The Vancouver Sun, 200 Granville St., Suite 1, Vancouver, B.C., V6C 3N3.

Secrets of building a solid nest egg in real estate

|

|

|

Michael Kane |

|

Vancouver Sun |

Friday, November 18, 2005

|

|

|

|

Debbie and Dennis Nisbet built their current real estate wealth of about $2.7 million over 20 years, mostly using other people’s money.

They say you can do it, too, if you are prepared to be frugal, take some calculated risks and ride out periodic down markets.

For example, Dennis Nisbet paid $135,000 for his first investment property in 1982, only to watch its value fall back to about $120,000, before climbing to $200,000 by 1988.

In 1996, the Nisbets paid $625,000 for their waterfront home in Port Moody, and spent “a few tough years” wondering if they would have to sell it to keep their heads above water. Just nine years later, the home is valued at $1.4 million.

They advise clients to shun townhouses and condominiums in favour of pre-owned single-family homes with basements, preferably above-ground, that can be rented out.

The Nisbets say 25 per cent of the value should be in the structure, and 75 per cent should be land. “That’s the perfect formula, because the land always increases and the structure decreases,” Dennis Nisbet said.

When the buyers have built some equity, they can borrow against it to buy a second home, usually within three or four years, and then continue buying indefinitely.

Last week’s Smart Money detailed a strategy to preserve retirement capital and provide income over 10 years, a period covering both a bull market and a bear market in financial securities. Over the same decade, the Lower Mainland saw a bear market in real estate, followed by the current bull market.

Dennis Nisbet says investing the same $100,000 in real estate over the same period — as they did in Maple Ridge in 1994 — would have put you streets ahead of investing in a Canadian balanced mutual fund.

Here’s how it worked. Had you invested $100,000 to buy a $160,000 property, you would have needed a mortgage of $60,000. The rental income of $1,500 monthly would have paid all of your expenses, plus a management fee of $150 monthly, and paid you about $600, similar to the income from the mutual fund.

By 2005, the property was worth $340,000. Assuming the mortgage was still $60,000, your equity had increased to $280,000. Your rental income would have grown to about $1,800 monthly, which would pay you close to $900 monthly after expenses.

If you sold the property, you would receive your initial $100,000, plus a taxable gain of $180,000. During this time, your income, averaging $750 monthly, would have totalled $90,000. The same $100,000 invested in the average Canadian balanced fund would have paid you $7,700 in taxable gain and an income of $69,960.

The real estate advantage, Nisbet says, is $20,040 more income and $172,300 in additional wealth. And that’s assuming you paid $18,000 to have someone else manage the property, something the Nisbets say you could probably do yourself.

So why do most people limit real estate investing to their own personal residence?

“We often find that first-time buyers, younger people, don’t want to start off with tightening their belts,” Debbie Nisbet says.

“They are used to having a new car, whether it is leased or bought new, and they want a brand new apartment or a newer house, and they want it in Vancouver or Burnaby or Coquitlam. When they can’t do it, they don’t do anything. They don’t want to start at the bottom and work their way up.”

Dennis Nisbet says their own children are all self-sufficient and talking about getting their first investment properties. “We are not at all enabling parents,” he said.

© The Vancouver Sun 2005