Province

With sales increasing in more than half of 11 markets surveyed, Re/Max is saying that the worst of the recession is over for the housing industry. — NATIONAL POST

OTTAWA — The worst is over in the Canadian residential-housing market, according to a new industry report that forecasts growth in the sector in the fourth quarter of the year.

According to the Re/Max Bricks and Mortar Report, “the bounce-back that began in early spring has made this recession one of the shortest on record for real estate.”

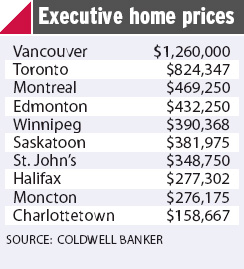

With Vancouver leading the way, sales increased in more than half of the 11 markets surveyed, and values have surpassed “recordbreaking” 2008 levels in seven of the markets.

“The strength of the residential-housing sector cross-country has taken many economists and housing analysts by surprise once again,” said Elton Ash, regional executive vice-president, Re/Max of Western Canada.

“In terms of its impact on the resale market, by historical standards, this recession was one of the mildest. . . . While there may still be some challenges down the road, the worst is definitely behind us in the housing industry.”

Low interest rates and falling housing prices in the midst of the economic downturn helped drive sales growth, Re/Max said.

Sales in Vancouver, one of Canada’s most expensive housing markets, rose 14 per cent from January to August, while sales were up 7.4 per cent in Victoria over that period, 6.2 per cent higher in Edmonton and up five per cent in Regina.

In Ottawa, where the real-estate market remained fairly steady through the economic crisis because of the city’s relatively stable employment situation, sales were up 2.4 per cent.

Nationally, the average price of a home is about $312,585, up 0.5 per cent from January to August, but there was a much larger jump in St. John’s, N.L., where the average price rose 18.1 per cent to $203,584.

There have also been substantial increases in Regina (6.4 per cent), Halifax-Dartmouth (3.5 per cent), Winnipeg (3.5 per cent) and Ottawa (3.3 per cent).

“Prices are on the upswing and inventory levels are tightening, so the push toward home ownership is expected to continue throughout the fall and possibly into early 2010,” says Michael Polzler, executive vice-president, Re/Max Ontario-Atlantic Canada.