Other

Archive for September, 2013

What Happens When the Boomers Sell Their Houses?

Thursday, September 5th, 2013Angie Oshika

Other

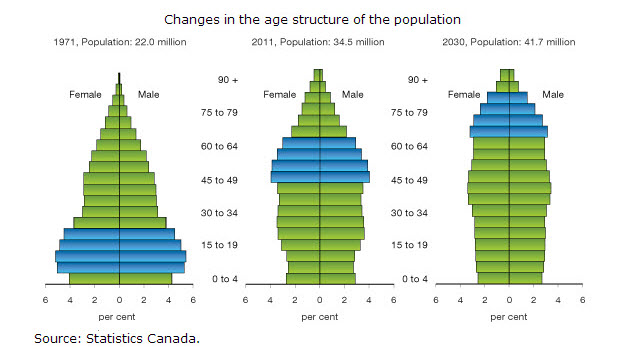

Imagine a flood of houses suddenly listed for sale across Canada, overwhelming supply and causing prices to drop dramatically. That’s the nightmare scenario that some real estate analysts predict. And the source of this sudden flood? The generation of Canadians known as the Baby Boomers reaching retirement and downsizing.

The Boomers make up almost one-third of our population (29%), and as they’ve moved from one life stage to the next, their needs have always shifted our society. So should we fear that this time they’ll topple the entire real estate market and ruin the financial future of the generations that follow?

Probably not.

Recent studies by the Conference Board of Canada and Royal LePage suggest that the situation isn’t as clear cut as the demographic charts might make us think.

Boomers don’t always follow the path of previous generations. They’re approaching retirement with more ambition, better health, and more affluence. In fact, the Royal LePage study reports that nearly half (43.5%) of Boomers who plan to move intend to find a new home that is the same size or bigger than their current one. Phil Soper, Chief Executive Officer of Royal LePage Real Estate said, “Baby Boomers are the wealthiest generation in Canadian history. They live in large homes with ample space for their many possessions. They love their garages and their yards.”

Adult children are staying at home longer, too – as many as 33.4 percent in some provinces. Soper explains, “The adult children of Baby Boomers aren’t going anywhere fast. Good jobs have proven more difficult for them to find, they’re extending their studies and they’re living at home. It is no wonder the concept of swapping a family-sized home for a small retreat has lost its lustre.”

When Boomers do start to move to smaller dwellings, will there then be an absence of interested buyers for multi-story houses? It doesn’t look that way.

The children of the Boomers, known as Generation Y, are a substantial subset (27.3%) of the population themselves. As they settle and start families, the perceived safety and comfort of the multi-story homes in the suburbs is appealing and familiar. The study is clear, Soper explains: “… the study results do not point to a … decrease in demand for traditional single-family homes. For the Baby Boomers that do head downtown, there is a generation waiting to move in.”

Another factor is international immigration: new Canadians will also be looking for safe neighbourhoods with parks and schools nearby. In addition to this increase in demand, construction of new single-family homes is expected to decrease, and some of the existing houses will be converted into multiple-unit dwellings. Single-family houses will become somewhat rarer.

As we can see, the formula isn’t as simple as predicting what the aging Boomer generation will do. The market for smaller homes is just as complex. The Conference Board of Canada study points out that a percentage of Boomers will downsize, thereby increasing the market for condominiums and townhomes. One-person households are growing as well, because of more divorces and fewer couples and families being formed. That adds to the demand for multifamily units, particularly in urban centres.

But both studies agree that a wide range of market and demographic factors will contribute to keeping our real estate market cushioned and homes of all sizes selling as the Boomers settle into retirement.

© 2013 Real Estate Weekly

Residential REITs take a hit

Tuesday, September 3rd, 2013Some look to development, U.S. market as higher mortgage rates gut share values

FRANK O’BRIEN

Other

Rising mortgage rates have cooled a five-year run of acquisitions – and rising share values – of real estate investment trusts (REITs) in the residential market.

Share prices of five residential-focused REITs surveyed show all have seen sharp declines since May when lending rates began to move upward. As of press time, the average for a five-year closed mortgage among the big Canadian banks was 4.26 per cent. This compares with sub-3 per cent rates a year ago for REITs that access Canada Mortgage and Housing Corp. insured mortgages.

Mortgage payments are the single largest cost for most residential REITS.

“It’s all about interest rates,” said REIT analyst Heather Kirk of BMO Capital Markets. “There is concern about where rates are headed.”

Residential REITs primarily focus on buying and, if necessary, selling rental apartment buildings. Traditionally, REIT acquisition managers look for larger buildings – 100 units or more – or portfolios of buildings, and are usually buying for a longtime hold.

However, the drop in share values – down an average of 13 per cent since May – is convincing some REITs to unload property.

Calgary-based Boardwalk REIT is among them.

“We believe Boardwalk shares are undervalued,” said Bill Chidley, the company’s senior vice-president of development, in explaining that Boardwalk plans to sell some of its assets and buy back its shares. As of press time, Boardwalk unit shares were selling for $58, down from $66 a year earlier.

Rumours are rife that Boardwalk is about to list some or all three of its highrise concrete rental buildings in Burnaby and Surrey, though Chidley said, “We have not determined which properties will be sold.”

Low cap rates

It would make sense to sell into the current Metro Vancouver market, said David Goodman, a multi-family property specialist with HQ Realty Services Ltd., who notes that apartment-building prices are at or near record highs while capitalization rates are near historic lows.

A price example: Goodman recently sold an old, 10-unit East Vancouver walk-up rental building for $185,000 per door and a cap rate of 2.1 per cent.

A pullback by REITs could further soften a Metro market that has seen a decline in sales and a rise in vacancies in recent months, he suggested – just don’t expect REITs to be buying much this year, though.

“Acquisitions are much more difficult today [because of higher lending rates],” according to Chidley.

The evidence is clear. Northern Property Real Estate Investment Trust (NP REIT), which capped a $130 million acquisition binge last year with purchases of apartment buildings on Vancouver Island and in the Fraser Valley, has not bought a single property so far in 2013. Instead, the Calgary company is looking at becoming a rental developer, seen in its purchase last year of three parcels of raw land.

“The exceptionally high asking prices for existing apartments have created a climate where construction of new multi-family residential property is possible,” NP REIT said in a recent release.

So far, NP REIT has about 600 units under construction, including its first rental project in Regina, and is currently trading at $27.27, down from $33 a year ago.

Giant landlord Canadian Apartment Properties REIT (CAP REIT), which holds 38,000 rental units, has bucked the acquisition trend with the purchase of six apartment buildings in Calgary so far this year. Last year, five Victoria apartment buildings were among record acquisitions by the Toronto-based company, which also included a mobile home park portfolio.

CAP REIT is trading at $21.40, down from $26 from a year earlier, as of our August 1 press deadline.

U.S. play

Another aggressive buyer is Vancouver-based Pure Multi-Family REIT LP, the only Canadian REIT focused exclusively on the apartment rental market in the United States. In July, Pure bought a resort-style, 264-unit Dallas, TX, rental complex on 10 acres for US$16.5 million. The numbers look good: Pure paid US$62,500 per door and accepted a cap rate of 6.9 per cent.

“These units rent for $1,000 to $1,500 per month,” said a spokesman for Pure, which so far this year has bought four Texas rental properties for a total of $104 million, with an average cap rate of 6.46 per cent, and is trading at $4.40 per share, down from $5.50 a year ago.

The U.S. rental market has some advantages over Canada, analysts note. These include:

• demand from millions of former homeowners who went into foreclosure;

• a strengthening U.S. economy;

• low prices in most urban markets; and

• a tax system that allows property owners to escape capital gain taxation when they sell an apartment building.

Since the U.S. housing crash in 2008 the number of households renting has jumped to 38 million and is expected to ramp up to 41 million in the next two years, according to the U.S. Census Bureau.

from Western Investor September 2013